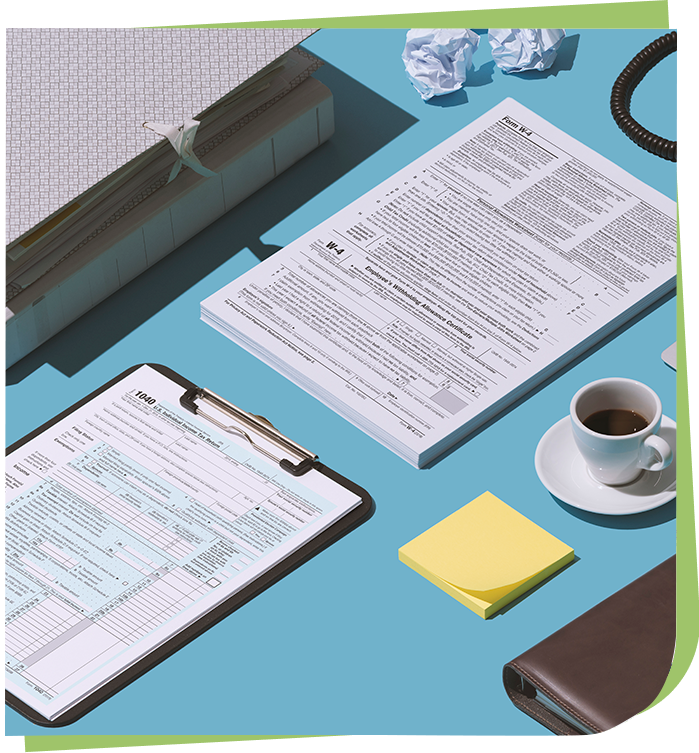

Tax Returns for Businesses & individuals

Taxleaf has been helping businesses, families, and individuals with their taxes since 1976. Let us show you why experience matters most when planning for your future.

Create a New COMPANY Today

Let the Business Specialists help you create a new company for your Business. A few minutes with us might save you a ton for years to come.

BOOKKEEPING + PAYROLL

Starting at $199/month

Build your own accounting package for your business by answering just a few questions about your business. We guarantee it will be the best decision you will ever make for your business.

Helping Non-Residentsinvesting in USA

If you live outside the USA and plan to do business in the USA, make sure you give us a call. We love to help non-residents with their business needs here in the states.